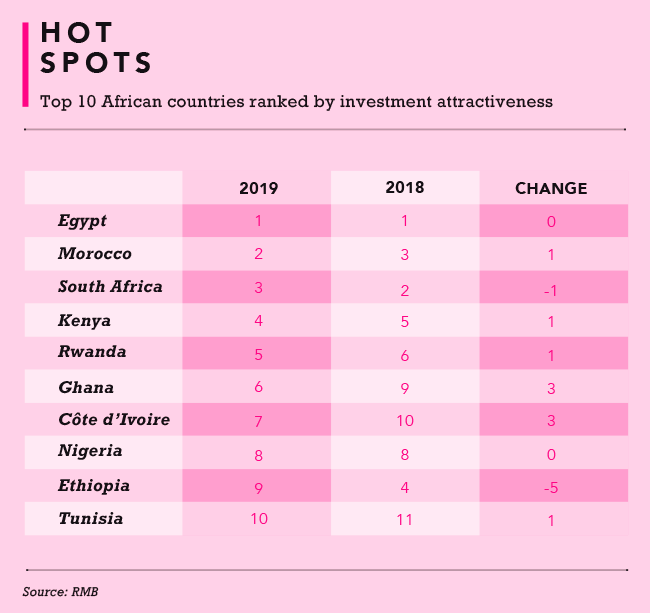

Egypt, Morocco, South Africa. These were the three nations earmarked by Rand Merchant Bank (RMB) as the African countries to watch in terms of investment this year. Mining, manufacturing, retail, construction, technology and telecoms were the sectors that could prove lucrative, says RMB in its Where to Invest in Africa 2020 report.

Investment firm RisCura has long followed the approach of segmenting Africa into meaningful regions when creating analytical models for investment. It is an important exercise, the company says, due to the range of ‘distinct investment destinations, each with its own attractions, flaws, cultural differences and business practices’. In its Bright Africa 2019 report, the company grouped investment destinations into the Maghreb region, Egypt and Sudan, francophone West Africa, ‘other’ West Africa, Nigeria, East Africa, Central Africa, Southern Africa (excluding South Africa) and South Africa.

RisCura notes in the report that trade within Africa remains poor, seeing that two-thirds of African imports come from Europe and Asia, and intra-continental trade accounts for just 13% of all African imports. This was set to improve with the African Continental Free Trade Agreement (AfCFTA), which was to come into effect in May 2019. The AU, however, decided to postpone the implementation of AfCFTA to 2021.

The WEF has referred to the trade agreement as ‘perhaps the most ambitious free-trade project since the WTO itself’. By reducing barriers to trade, the economic prospects for the entire continent will be boosted. ‘If Africa was to increase its share of global trade from 2% to 3%, the one percentage point increase would generate approximately US$70 billion of additional income per year for the continent,’ according to the WEF. That, however, was all pre-COVID.

Statistics and analysis from mere months ago today seem like they could have been lifted from reports dating back a decade. The situation has changed overnight, and drastically so. Already struggling economies and industries have been dealt further blows by the economic fallout from the pandemic, as has been the case throughout the world.

Ngozi Okonjo-Iweala, former Finance Minister of Nigeria, talking to the WEF, said she fears the COVID-19 pandemic could wipe out two or three decades of growth and development on the African continent.

The pandemic and the oil-price shock are likely to tip Africa into an economic contraction in 2020, in the absence of major fiscal stimulus, notes McKinsey in an article on tackling COVID-19 in Africa. The company stresses that bold, creative steps are needed to secure supply chains of essential products, contain the virus, and provide a sense of stability to financial systems. However, reformative actions by African decision-makers, such as the strengthening of intra-African trade and manufacturing, planned before the pandemic still hold water.

What COVID-19 has provided African countries with is the opportunity to reconsider the intra-African market and their dependence on Europe and other markets, says Abdou Diop, managing partner at Mazars Morocco. For the most part, Africa has taken measures to support lower-income segments of the population and the informal sector by introducing financial life rafts such as solidarity funds, but specific aid measures for the middle class are still lacking.

‘There are not enough measures in place to help the impacted business sectors to rebuild themselves in the long term,’ he says. Diop adds that policymakers must be proactive in finding the liquidity that can help relaunch Africa’s economies and local industries.

Along the same line of reasoning, the WEF notes that while there is not much to do about the current trend of deglobalisation and protectionism, the continent can embrace a self-supportive regionalism through enhanced intra-African trade.

‘Almost counter-cyclically, actively promoting trade liberalisation to encourage new areas of growth would be a pragmatic response to the reduction in global trade, not to mention promoting Africa as an enhanced destination for investment from multinationals,’ the WEF states.

Take, for example, the Chinese companies investing in Ethiopia viewing the nation as a supply-chain hub to the rest of the world. Morocco, Kenya, Egypt and South Africa, generally African countries with developed economies, can also prosper from building similar partnerships with China, says Diop.

This can help spur Africa’s integration into the global value chains for the automotive, aeronautic, textile and various other industries. Countries with accommodating business environments and with a geographical connection to global markets will be a key focus for investors, he explains.

Egypt in North Africa ticks these boxes, according to RMB’s report. ‘The enormity of the market size (which ranks second to Nigeria in nominal terms) paired with a sophisticated business sector relative to neighbouring countries, makes Egypt the most attractive investment destination in Africa,’ the report states. The country leaped eight places in the World Bank’s latest Ease of Doing Business rankings.

Challenges of depressed growth levels and lack of structural reform aside, South Africa remains Africa’s hotspot for portfolio investment, says RMB. ‘With many African nations facing severe liquidity constraints, South Africa’s financial markets and level of financial inclusion are still a cut above the rest.’ However, questions of corruption at executive level and other issues with its SOEs remain.

According to Deloitte in an article on investing in Ethiopia and the structural reforms set to unlock East Africa’s largest economy, Ethiopia is one of the world’s fastest-growing economies. Between 2008 and 2018, it recorded an average real GDP growth rate of 9.9%. ‘This broad-based high growth rate has been supported by structural reforms that have been introduced through industrial sector development.’ Prime Minister Abiy Ahmed announced numerous reform initiatives, including plans to loosen the state’s dominance in key sectors in efforts to attract investor interest and boost growth. ‘The government has been successful in nurturing the country’s comparative advantage (agriculture and manufacturing),’ states RMB. ‘And with almost 100 million people, the demand for goods and services is rising significantly.’

It notes that without sustainable funding and commercial credit, project development in key areas such as infrastructure, healthcare, and energy projects remain concepts rather than reality. ‘Regulatory reforms, the emergence of an urban middle class and technological advancements allow financial institutions access to funding mechanisms to mitigate risk and maximise returns.’

Just as Africa recently realised its over-reliance on China-based supply chains (Diop points to a shortage of Chinese-imported rice in many African nations), European countries and the US are coming to the same realisations – remember the surgical mask shortage in the US due to issues with imports from China, which made half the world’s masks before the coronavirus emerged there? This creates opportunities for Africa to serve as a substitution to Chinese-manufactured goods, says Diop.

With Africa being strategically located, this potential shift by Western companies won’t necessarily be a cost-driven decision.

Before COVID-19, the partnership between China and Africa was based on the diversification of international partnerships for Africa, as it became increasingly complicated for the continent to deal with Western powers and demands that were tied to aid and investment, according to Diop. ‘Post-COVID-19, there will be a change in mindset, as Chinese companies will increasingly need to be closer geographically to their customers in Europe and the US, which is an excellent opportunity for African companies.’ Companies able to create ‘hubs’ for Chinese companies to settle in these regions, will benefit greatly from investment. ‘COVID-19 will allow a new deal in the relation between some African countries and China.’

As Cesar Augusto Mba Abogo, Equatorial Guinea’s Minister of Finance, Economy and Planning, explains in an editorial published by the WEF, several African countries made important policy decisions to define and prioritise national development aspirations in alignment with the UN’s Agenda 2030 and the AU’s Agenda 2063. ‘And then, COVID-19 arrived,’ he says.

The minister is certain that opportunities will emerge, adding that ‘innovative minds, previously imprisoned by institutional inertia and interest groups, will rise to the challenges that we collectively face’.

There’s a certain phoenix from the ashes sentiment taking hold across the world at present. That maybe if we have little left to lose, where lies the harm in implementing radical changes for the better?

‘Africa needs to re-imagine and rethink itself,’ Okonjo-Iweala told viewers in a World Bank podcast. ‘And I think we can use this as an opportunity. I see that out of this crisis, we can really make many good things.’

By Sven Hugo

Images: Reuters/Gallo Images